China Shipping Market Update: March 2026

February 2026 was a soft market: falling spot rates, predictable CNY disruption, and manageable surcharges. March is the opposite. The US-Iran military exchange on February 28 triggered a chain reaction across ocean freight, air cargo, insurance markets, and port operations. If the situation does not resolve quickly, the effects are likely to extend through the end of Q1 and into April.

Five market shifts define March 2026 for China importers. This update covers what has changed, how conditions are expected to develop through the month, and what operational decisions need to be made now.

March 2026 Market Snapshot

Hormuz closure: Major P&I clubs have suspended war risk cover for the Strait of Hormuz and Persian Gulf; commercial vessel transits have stopped

Cape of Good Hope rerouting: All Asia-Europe and Asia-Middle East services now bypass both the Red Sea and the Gulf, absorbing 15-20 days of additional transit time per round trip

Air freight rates: Spot rates on China-Europe routes have risen 40-60% since February 28 due to airspace restrictions and demand switching from sea to air

War surcharges: War Risk Surcharge (WRS) and Emergency Conflict Surcharge (ECS) of $1,500-$3,000 per TEU are being applied industry-wide on Gulf-touching lanes

Hub congestion: Singapore, Colombo, and Indian west coast ports are absorbing diverted volumes, with 3-5 day additional dwell times already reported in early March

Update 1: Hormuz Strait Effectively Closed to Commercial Shipping

Iran announced restrictions on commercial vessel passage through the Strait of Hormuz following the February 28 strikes. The commercial impact has been immediate and near-total, for one reason that goes beyond the military threat: insurance has collapsed.

All major Protection & Indemnity (P&I) clubs, including the International Group of P&I Clubs which covers approximately 90% of the world's ocean-going tonnage, have suspended or withdrawn war risk coverage for the Strait of Hormuz and the broader Persian Gulf zone.

Without valid war risk insurance, vessels cannot legally transit under the terms of their financing agreements, port state requirements, and cargo contracts.

Carrier responses entering March:

Maersk, MSC, CMA CGM, COSCO, and Hapag-Lloyd have all issued operational notices suspending Gulf port calls. Affected ports include:

Dubai (Jebel Ali)

Abu Dhabi (Khalifa Port)

Dammam (King Abdulaziz Port)

Muscat (Port Sultan Qaboos)

Vessels that were en route to Gulf destinations as of February 28 are holding in anchorage outside the Strait or diverting to Colombo and Singapore for cargo repositioning decisions.

Based on current conditions, a near-term resolution within March appears unlikely. Insurance market re-entry, the practical precondition for vessel resumption, requires a verified ceasefire followed by a P&I reassessment period of at least 2-4 weeks. Gulf port calls resuming in March would require a rapid de-escalation that is not currently in sight.

Jebel Ali, as the Middle East's largest container hub and a critical transshipment point for onward cargo to Pakistan, India, and East Africa, is now operating on inbound cargo from existing anchorage stock only. No new vessel arrivals from Asia are anticipated until the insurance situation changes.

Update 4: Surcharges Now Rival Base Freight on Affected Lanes

The March 2026 freight bill looks structurally different from anything seen in the past two years. On lanes touching the Middle East or routing via the Cape of Good Hope, surcharges are no longer marginal line items. On some routes, they now exceed the base ocean freight charge.

War Risk Surcharge (WRS): Applied by all major carriers to any service that was previously routed via the Gulf or Red Sea, or that calls at ports in the affected region. Current WRS rates being quoted range from $1,500 to $3,000 per TEU depending on carrier and specific port of destination. In our own operations, we have seen WRS charges reach $3,000 per TEU on Gulf-destined containers booked in early March.

Emergency Conflict Surcharge (ECS): A separate temporary charge being applied by several carriers to cover operational contingency costs including vessel repositioning, crew security arrangements, and port disruption handling. ECS rates are $300-$700 per TEU where applied.

Bunker Adjustment Factor (BAF): The Brent crude price has moved above $100 per barrel following the conflict. Carrier fuel surcharge mechanisms are adjusting on weekly rather than monthly cycles. Expect BAF increases of $200-$400 per FEU on long-haul routes within the next 2-3 weeks as current hedging positions expire.

EU ETS (unchanged but more visible): The $75-$150 per FEU EU carbon surcharge established on January 1, 2026 remains in place on Europe-bound cargo. At the higher freight rates now prevailing, the percentage impact is smaller, but the absolute cost is unchanged.

Illustrative total cost example for a standard 40ft container, China to Rotterdam:

Base ocean freight: ~$3,500 per FEU

War Risk Surcharge: $2,000 per FEU

Emergency Conflict Surcharge: $500 per FEU

Bunker Adjustment Factor: $800 per FEU

EU ETS carbon fee: $135 per FEU

Total indicative cost: ~$6,935 per FEU

This compares to approximately $2,400-$2,600 per FEU (base plus ETS only) in February. Importers who locked annual contracts in January 2026 at rates 20% below 2025 levels now face a situation where surcharges may trigger contract re-negotiation clauses or force spot-market decisions.

Request a complete surcharge breakdown from your freight forwarder before confirming any booking. The base rate is no longer the primary cost driver on Gulf-adjacent and Europe lanes.

Update 3: Air Freight Rates Rise 40-60% on Airspace Closures

The Middle East functions as the primary transit hub for air cargo between Asia and Europe, Africa, and parts of South Asia. Iranian, Iraqi, Kuwaiti, and parts of UAE airspace have been restricted or closed to civilian overflights since February 28. This has disrupted the routing of cargo aircraft in two compounding ways:

Direct flight paths are broken. Flights from China to Europe, East Africa, and parts of South Asia that previously transited Middle Eastern airspace now require significant rerouting, adding 2-4 hours of flight time and corresponding fuel costs per sector.

Demand has shifted from sea to air. Importers with time-sensitive cargo originally destined for Gulf ports, now inaccessible by sea, are exploring air freight as an alternative. This demand surge is hitting a market where capacity is already constrained by rerouting.

Indicative air freight rates for March 2026:

China to Europe (general cargo): $6.50-$8.50 per kg, up from $4.00-$5.20 per kg in mid-February

China to Middle East: Limited flights available; rates where operational are $7.00-$9.00 per kg with ongoing route uncertainty

China to US (via polar route, unaffected): $4.50-$5.50 per kg, modest increase driven by demand overflow

Emirates SkyCargo, Qatar Airways Cargo, and Etihad Cargo, which together handle a significant share of Asia-Europe air cargo volumes, have suspended or significantly reduced services due to airspace and ground operation uncertainty at their hub airports.

Air freight is available for China-to-Europe movements via northern routing (polar or Central Asian corridors), but capacity is limited and lead times for bookings have extended to 5-7 days where they were previously 24-48 hours. For urgent cargo, secure bookings as early as possible.

Update 2: Asia-Europe Routes Fully Rerouted via Cape of Good Hope

The Suez Canal resumption that eased capacity pressure in early 2026 has been reversed. With both the Red Sea (Houthi threat, unchanged since 2024) and the Strait of Hormuz (new, war-related) now effectively closed, every major carrier has committed all Asia-Europe and Asia-Middle East services to Cape of Good Hope routing.

This is not a partial rerouting. As of March 1, no major alliance service is using the Suez Canal or transiting the Gulf.

Capacity absorption at scale:

The Cape of Good Hope adds 15-20 days to round-trip voyage times compared to Suez routing. On a vessel completing four round trips per year under normal Suez conditions, Cape routing reduces that to roughly three round trips annually. In practical terms, this removes 20-25% of effective Asia-Europe capacity from the market without a single vessel being scrapped or delayed in delivery.

The 2026 new vessel delivery schedule, which was forecast to create significant overcapacity and sustained low rates, is now largely offset by this rerouting effect. The rate softness seen in February has begun to reverse.

There is a second factor compounding this capacity pressure in March specifically. Chinese New Year fell in mid-February, and factories entered full post-holiday production in late February and early March.

March is the first concentrated shipment window of the year, when suppliers across the Pearl River Delta and Yangtze River Delta release accumulated orders simultaneously. In a normal March, this surge in cargo volume meets a market with adequate vessel space.

In March 2026, it meets a market where 20-25% of effective Asia-Europe capacity has been absorbed by Cape rerouting. The practical result is not only higher rates but genuine space shortages on Europe and Middle East lanes. Rolled bookings and extended lead times are a realistic outcome, not just surcharge adjustments.

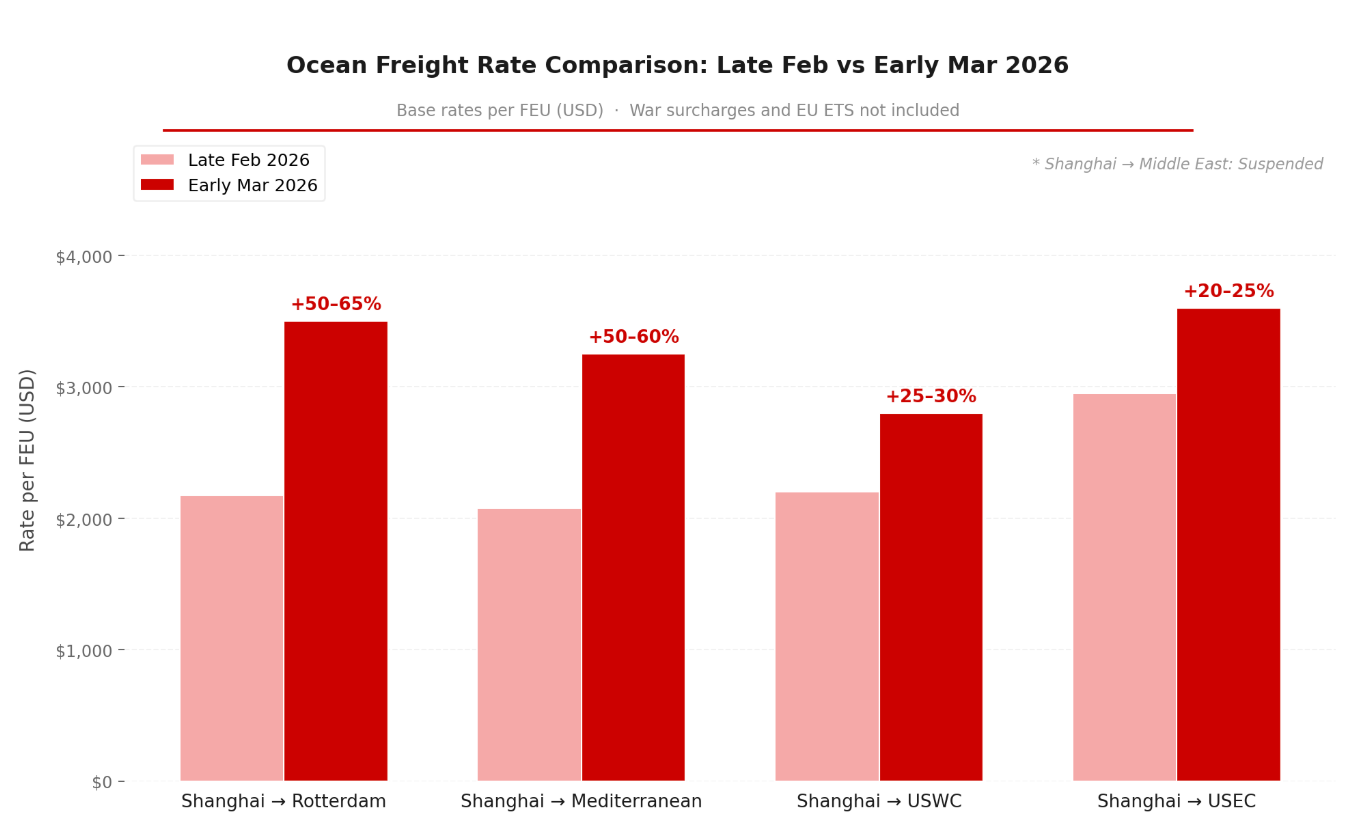

Rate trajectory for March:

Spot rates on Asia-North Europe lanes entered March sharply higher than February levels, with indicative rates of $3,200-$3,800 per FEU on Shanghai to Rotterdam and $3,000-$3,500 per FEU on Asia-Mediterranean. These figures are directionally correct but should be verified with your freight forwarder at time of booking, as the market is repricing weekly.

If the conflict continues through March without resolution, rate pressure on Europe lanes is likely to be sustained. Blank sailing reductions from February are still unwinding, and the capacity absorbed by Cape rerouting is not offset by any near-term schedule changes. There is limited structural basis for Europe rates to retreat meaningfully within March.

Transpacific rates have followed a different path. USWC lanes, which are unaffected by Gulf or Red Sea closure, are seeing demand pressure as shippers redirect cargo away from USEC services that require Suez transit. USWC rates have moved upward from February levels and may remain elevated through the month if the demand shift continues.

Note: These rates do not include war surcharges or EU ETS carbon fees, which are applied separately.

Update 5: Port Congestion Shifts to Secondary Hubs; USWC Absorbs Diverted US-East Volumes

Middle East hub displacement:

Jebel Ali (Dubai) handled approximately 14.8 million TEU in 2025, functioning as the primary transshipment hub for the Indian subcontinent, East Africa, and parts of the Gulf. Its effective closure to new vessel arrivals has displaced this transshipment volume onto secondary hubs that are not designed for this scale.

Singapore is experiencing congestion as diverted Middle East-bound cargo seeks alternative transshipment points. Vessel dwell times have extended and the port authority (MPA) has requested advance cargo notification and pre-booking of berth slots. Congestion may worsen through mid-March if the volume of redirected vessels continues to build.

Colombo (Sri Lanka) is absorbing India-subcontinent and East Africa transshipment volumes previously handled through Jebel Ali. Yard utilization is running at approximately 85% and may tighten further as March progresses.

Indian west coast ports (Mundra, JNPT/Mumbai) are receiving increased direct-call requests from carriers previously routing via Jebel Ali. Both ports have limited reefer plug capacity and yard space, which is a specific constraint for cold chain importers moving pharmaceutical or food cargo.

US West Coast rebalancing:

For China-to-US cargo, the route disruption is minimal, but capacity allocation is shifting. USEC services that previously transited Suez are now rerouting via Cape, adding 10-14 days per voyage. This makes USWC comparatively more attractive for importers with flexibility on port of entry.

Los Angeles and Long Beach may see increased vessel queue times from mid-March onward. The demand shift from USEC to USWC takes several weeks to materialize in port operations, as vessels booked in early March begin arriving simultaneously around March 15-20. The relative stability of USWC rates in early March does not necessarily indicate the lane will remain uncongested for the rest of the month.

For importers with East Coast distribution requirements, the question of whether to reroute via USWC with inland rail or truck is worth evaluating before mid-March. If LA/Long Beach queue times extend later in the month, the logistical advantage over a Cape-routed USEC service may narrow.

Frequently Asked Questions

What should I do if I have cargo currently en route to a Gulf port?

Contact your freight forwarder immediately. Options are transshipment at Colombo or Singapore, diversion to an Indian west coast port, or return to origin. Demurrage costs at anchorage accumulate quickly, so decisions cannot be deferred.

How long will the Hormuz closure last?

There is no reliable timeline. P&I clubs require a verified ceasefire plus a minimum 2-4 week reassessment period before reinstating war risk cover. Plan all March and April Middle East shipments on the assumption that Gulf sea freight will not resume within this quarter.

Are there alternative routing options for cargo destined for the UAE or Saudi Arabia?

Oman's Port of Salalah, outside the Strait, can receive cargo for onward truck delivery into the Gulf for non-urgent shipments. Air freight via surviving flight routes is the primary option for time-critical cargo. Discuss specific requirements with your forwarder before committing.

Do war surcharges apply on top of my January annual contract rate?

Yes. Standard contract terms allow carriers to levy surcharges arising from extraordinary events that were not in scope at the time of rate negotiation. WRS, ECS, and BAF adjustments are not capped by annual contract rates on any major carrier's standard contract terms.

Should I switch China-to-Europe shipments from sea to air?

Only for high-value, time-sensitive cargo where delay cost exceeds the air freight premium. At $6.50-$8.50 per kg, air freight is not economical for standard manufactured goods. For pharmaceutical, DG chemical, or semiconductor shipments, the calculation may justify it on a case-by-case basis.

Conclusion

The February 2026 shipping environment, characterized by falling rates and controlled disruption from CNY-Ramadan overlap, ended abruptly on February 28. March 2026 presents a fundamentally different operating context: war-driven route closures, insurance market failure in the Gulf, and surcharge structures that have doubled or tripled total freight costs on affected lanes within days.

For China importers, the immediate priorities are cargo in transit to Gulf ports, forward bookings on Europe lanes where rates are rising rapidly, and air freight alternatives for time-critical shipments. The Transpacific remains the most stable major trade lane, though USWC capacity is tightening.

Gerudo Logistics is actively managing these disruptions for clients across DG, reefer, and general cargo categories. Our operations team in Guangzhou, Shanghai, and Shenzhen is coordinating alternative routing, surcharge transparency, and customs clearance support for March shipments.

Contact us for route-specific guidance, booking assistance, or an updated landed cost assessment for your March cargo.