China Shipping Market Update: April 2026

The Middle East conflict that began in late February continues to define the operating environment for China export shipping in April.

With the Strait of Hormuz commercially unviable for most global carriers and the Red Sea remaining closed to commercial traffic, Cape of Good Hope rerouting is the standard across Gulf and Europe lanes. Against this backdrop, a transpacific GRI has landed, US customs enforcement from late March is producing clearance delays at port, and new DG and cold chain operational developments are requiring immediate attention.

This briefing covers the key developments shaping China export shipping through April and into May.

April 2026 Market Snapshot

Five developments are shaping China export shipping this month:

Rate by lane: US lanes remain elevated following the April 15 GRI, driven by defensive booking ahead of potential May tariff action. Southeast Asia is tightening from hub congestion and a surge in China-origin chemical demand. Europe is easing week-on-week. The Middle East carries an elevated geopolitical premium on top of base freight.

US Customs: Three compliance developments are affecting April shipments at different stages: Section 232 full-value assessment in effect since April 6, CBP IOR verification producing clearance holds on arriving containers, and the CAPE system going live on April 20.

IATA DG Digital: A two-tier processing system is now in mandatory trial at Shanghai and Hong Kong cargo terminals, creating 24 to 48 hours of additional queue time for manual DGD filers.

New Route Middle East: A Zhengzhou-Dubai air freight service launched April 7 on Emirates SkyCargo 777F, three departures per week, with DG capability for e-commerce cargo including lithium batteries.

Reefer Shortage: Equipment availability is under simultaneous pressure from seasonal Southeast Asian fruit imports and elevated geopolitical surcharges on Gulf-bound services.

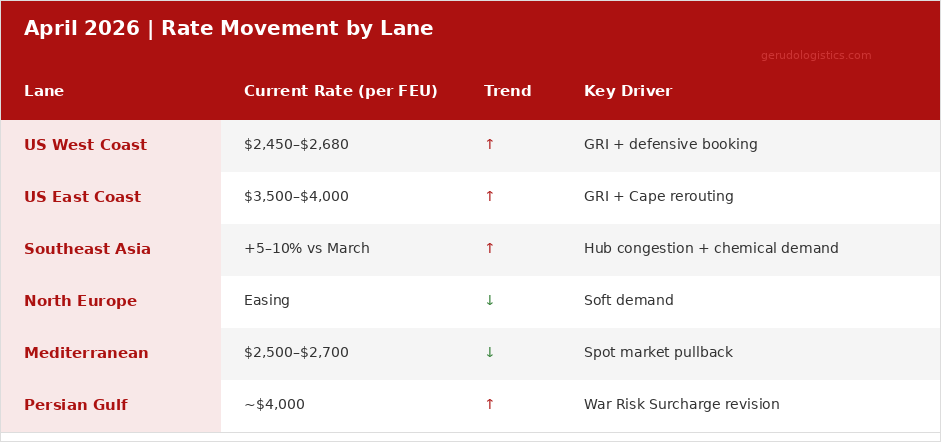

Update 1: Rate Movement by Lane

April is a diverging market. Transpacific lanes are the clear outperformer driven by tariff-related front-loading, while European routes are easing on softer demand. The Middle East carries a geopolitical premium that sits outside normal supply-demand logic.

April is a diverging market. Transpacific lanes are the clear outperformer driven by tariff-related front-loading, while European routes are easing on softer demand. The Middle East carries a geopolitical premium that sits outside normal supply-demand logic.

United States

West Coast rates are currently at $2,450 to $2,680 per FEU, and East Coast at $3,500 to $4,000 per FEU, with the East Coast carrying additional weight from Cape of Good Hope rerouting and seasonal port pressure. The April 15 GRI is already priced into quotes.

Following the Section 232 full-value tariff change on April 6, importers have responded with defensive booking ahead of potential May tariff action, compressing late-April availability significantly. LA/LB yard utilization has risen sharply, and inland rail connections to Chicago and Dallas are experiencing prolonged dwell times as concentrated arrivals exceed normal IPI throughput.

Southeast Asia

Near-sea lanes serving Vietnam, Indonesia, and Thailand are up approximately 5 to 10% in April. Singapore transshipment dwell times have roughly doubled due to tight East Asian capacity and accumulated backlogs, with carriers applying additional hub congestion surcharges from mid-April.

The Hormuz closure has separately cut off MEG and methanol supply to Southeast Asian manufacturers, driving a significant surge in China-origin chemical procurement and acute space tightness on specific DG services.

Europe

North Europe lanes are easing week-on-week, with the base rate decline partially offset by BAF, which remains the dominant cost variable under permanent Cape rerouting. Mediterranean ports including Genoa have pulled back to $2,500 to $2,700 per FEU as spot market pressure softens.

Rotterdam and Antwerp are enforcing a strict 7-day pre-arrival gate-in rule in response to vessel bunching from unpredictable Cape arrival windows. Exporters should confirm gate-in deadlines at the time of booking.

Persian Gulf

Gulf route rates are quoted at approximately $4,000 per FEU, with War Risk Surcharges under active upward revision as conflict conditions evolve. Jebel Ali is experiencing growing congestion from vessel capacity constraints and feeder delays, with onward transfers to Kuwait and Iraq now exceeding typical transit buffers. All Gulf surcharge rates should be confirmed at the point of booking.

Update 2: US Customs - Three Regulatory Developments

Three separate US customs developments are landing in April, each affecting a different part of the import process. Together they represent a meaningful compliance workload for importers with active China shipments this month.

Section 232: Full-Value Assessment in Effect Since April 6

The revised Section 232 tariff framework came into force on April 6, 2026, and the change is material for importers of machinery, special-purpose vehicles, and industrial equipment with significant steel or aluminum content. The new methodology applies the tariff to the full declared value of the finished product, rather than to the metal component value alone.

The practical actions required are time-sensitive:

Importers should recalculate their landed cost models using the new full-value assessment basis, as duty exposure on April arrivals may be significantly higher than previously calculated.

HS code classifications and tariff calculations should be reviewed with a licensed customs broker before the next shipment clears.

IOR Verification: First Wave of Clearance Delays at Port

CBP's strengthened Importer of Record (IOR) verification requirements came into force on March 20, mandating 100% real-time matching of IOR entity data against ACE system records. Containers that departed China in late March are now arriving through April, and those with inconsistent IOR data are encountering clearance holds.

The exposure is concentrated in specific arrangements:

DDP structures where a third-party logistics provider acts as the nominal IOR are most at risk, particularly where the provider's ACE-registered entity information has not been updated to reflect the March 20 requirements.

If a container is held on arrival, the resolution mechanism is a Single Transaction Bond, which resolves the immediate clearance issue but adds both cost and time.

Importers moving goods under DDP arrangements should verify IOR compliance with their provider ahead of the next shipment's arrival.

CAPE System: Action Required Before April 20

The Consolidated Administration and Processing of Entries (CAPE) system begins its first operational phase on April 20, 2026, affecting the drawback and entry processing workflow within ACE. A processing failure at cutover will delay entry acceptance and create demurrage exposure.

Importers and their customs brokers should verify that ACE filing logic is compatible with the new system before the cutover date.

One week of lead time is sufficient to address compatibility issues if the conversation with your broker happens now.

Update 3: IATA DG Digital - Paper Filings Are Now the Slow Lane

The IATA DG Digital system entered mandatory trial operation at major Shanghai and Hong Kong cargo terminals in early April. The system creates two processing tracks with meaningfully different throughput speeds, and the gap between them is now operationally significant for DG air shippers.

Shipments submitted through the digital pre-check channel move through a dedicated handling queue with priority access at the security and verification stage. Paper-format Dangerous Goods Declarations (DGD), by contrast, are processed through the legacy manual system, which is currently experiencing 24 to 48 additional hours of queue time during peak periods as the two-track system creates a backlog on the manual side.

In a high-frequency booking environment, this additional wait can result in missing a flight cycle and losing a day or more of transit time. Pre-registration on IATA DG Digital is now an operational necessity for lithium batteries, agrochemicals, and Class 3 and Class 8 products moving by air out of Shanghai or Hong Kong.

Update 4: Zhengzhou-Dubai Air Freight Corridor Now Operational

Emirates SkyCargo launched three weekly departures on 777F freighters from Zhengzhou to Dubai on April 7, 2026. The service is positioned primarily as a cross-border e-commerce corridor, with confirmed capability to carry DG cargo including lithium batteries under IATA DGR compliance. For e-commerce exporters and DG shippers based in or sourcing from central China, this route offers a direct air link to the Middle East that bypasses current sea route surcharges and the 20 to 25-day transit extension from Cape of Good Hope rerouting.

The practical considerations for this service:

The route serves the Middle East and onward to Europe, making it relevant for exporters targeting UAE-based distribution hubs.

Lithium battery shipments and similar DG e-commerce cargo must comply with IATA DGR requirements, including a correctly completed Dangerous Goods Declaration and packaging that meets air transport standards.

Capacity is limited at launch and should be secured early for shipments planned through May.

DG acceptance conditions vary by product and UN number and should be confirmed with the carrier before booking.

Update 5: Reefer Equipment Under Seasonal and Geopolitical Pressure

April marks the peak import season for Southeast Asian tropical fruits entering China. Inbound fruit trade is absorbing reefer equipment that would otherwise be available for China export cold chain services, creating a temporary but significant equipment tightness on outbound reefer lanes. This seasonal crunch is compounding the cost pressure already introduced by geopolitical surcharges.

The combined surcharge burden on reefer containers, incorporating War Risk, BAF, and equipment premiums, is running at elevated levels from major carriers including Hapag-Lloyd and CMA CGM. All current reefer rates should be confirmed at the point of booking rather than relied upon from earlier quotes.

For frozen food exporters, two options are worth evaluating:

Shifting bookings to late April onward, when the seasonal fruit crunch may ease and equipment availability may improve.

Assessing NOR (No-Operating-Reefer) containers where product temperature tolerances permit, to avoid the reefer equipment premium on base freight.

For Gulf-bound reefer cargo specifically, the Cape of Good Hope rerouting adds 20 to 25 days to transit times compared to a standard Suez routing. Before confirming any Gulf-bound reefer booking, the transit time must be evaluated against the specific product's temperature tolerance window. Where the extended transit falls outside acceptable limits, sea-air combinations via the Zhengzhou-Dubai corridor may be the more viable option.

How Gerudo Logistics Is Managing This for Global Importers

At Gerudo Logistics, we handle DG cargo under IATA, IMDG, and ADR compliance frameworks, and manage temperature-controlled shipments under full cold chain monitoring from origin through final delivery.

In the current environment, the difference between specialist handling and general freight management is measurable across three specific areas:

DG cargo to the Middle East: We assess carrier acceptance conditions against each shipment before confirming a booking, as acceptance policies on Cape-routed Gulf services are changing frequently. Every client receives itemized surcharge breakdowns with the relevant carrier documentation.

Reefer cargo routing: For frozen and temperature-sensitive cargo, we evaluate whether Cape of Good Hope transit times fall within the acceptable window for the specific product before confirming any Gulf-bound booking. Where transit times exceed product tolerance, we work through alternative routing options including air freight and sea-air combinations.

DG air freight via digital channels: For DG shipments moving by air out of Shanghai or Hong Kong, we file through the IATA DG Digital system to access the priority handling queue. Given current manual processing delays of 24 to 48 hours, this produces a measurable difference on time-sensitive bookings.

Conclusion

April is a month where the cost and operational risk of getting the details wrong is higher than usual. Surcharge levels are being revised on short notice, compliance deadlines are active, and equipment availability on reefer lanes is genuinely constrained.

Importers who confirm rates at the point of booking, verify IOR and ACE compliance ahead of arrivals, and pre-register DG air shipments through IATA DG Digital will avoid the most avoidable costs. We will continue to monitor developments and publish our next update in May.