Import Duties from China to Europe in 2026

A low tariff rate can still produce a high import bill. Goods entering the European Union may be charged customs duty, import Value Added Tax (VAT), trade defence duties and, for selected carbon-intensive products, Carbon Border Adjustment Mechanism (CBAM) costs.

Chemicals, frozen food, agricultural machinery and small parcels follow the same EU tax framework, although the information needed to confirm the rate differs. Chemical classification depends on identity and formulation, frozen food depends on species and processing, machinery depends on function and equipment type, and small parcels depend on product value and the applicable e-commerce procedure.

EU Import Taxes Overview

The European Union applies a common external customs tariff. The amount paid at clearance can still contain several separate tax layers.

Customs duty: The rate is based on the product's Combined Nomenclature and TARIC classification, origin, customs value and applicable tariff measures.

Import VAT: The rate and accounting method depend on the member state where the import takes place. The taxable amount is usually higher than the commercial invoice value.

Anti-dumping and countervailing duties: Selected products originating in China may face additional duties linked to the legal product scope and actual manufacturer.

Excise duty: Alcohol, tobacco and certain energy products may be subject to excise charges.

CBAM liability: Covered cement, iron, steel, aluminium, fertiliser, hydrogen and electricity products may create emissions reporting and certificate obligations.

Small parcel duty: From 1 July 2026, qualifying low-value distance-sale consignments with an intrinsic value of no more than EUR 150 are subject to a temporary EUR 3 customs duty per item.

Freight charges, customs brokerage, inspections, cold storage and destination handling should be listed separately from customs taxes.

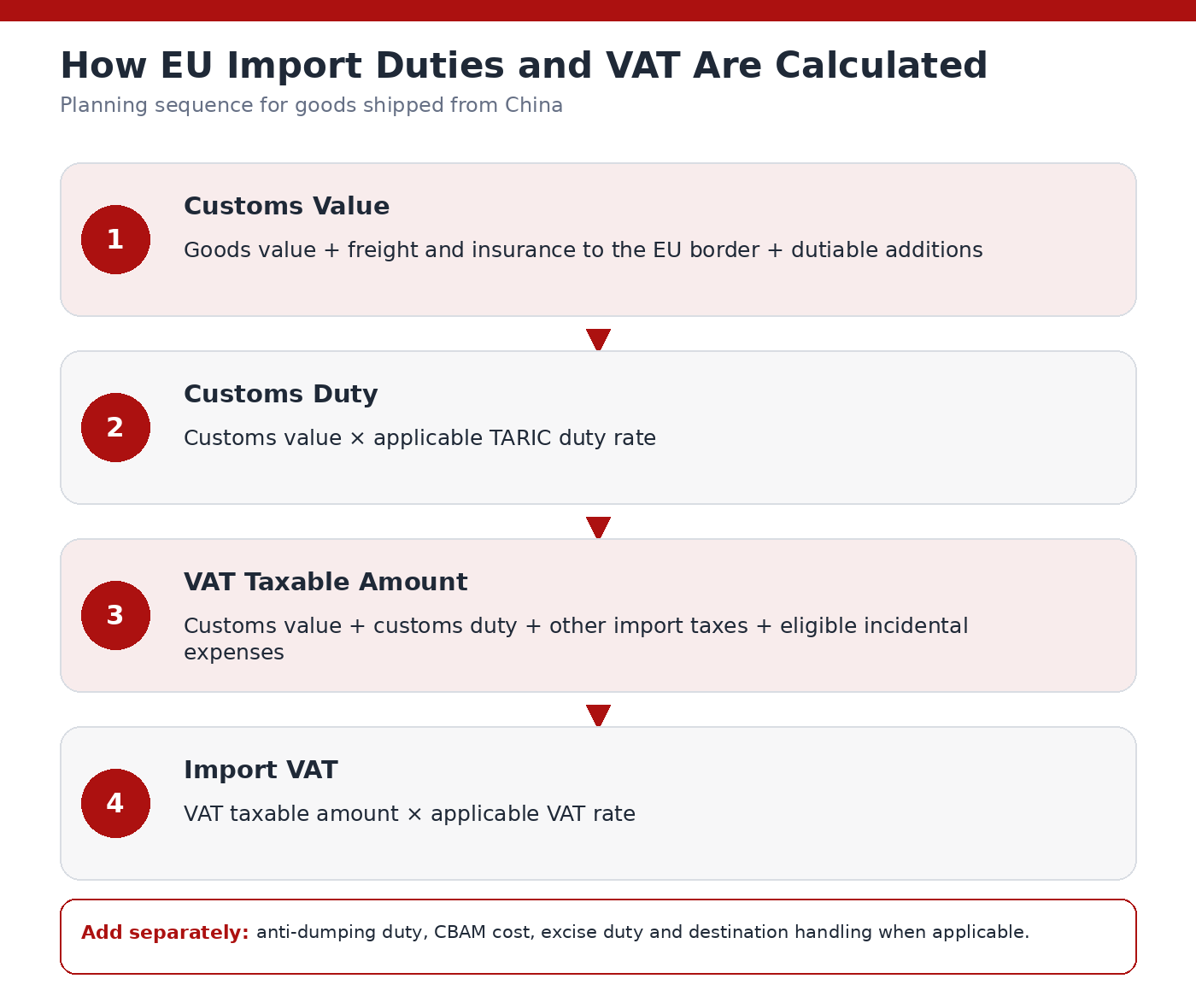

How EU Customs Duty and Import VAT Are Calculated

Customs duty is calculated from the customs value. Import VAT normally uses the customs value plus customs duty and other eligible costs.

Customs Value for Goods Shipped from China

The transaction value, meaning the price actually paid or payable for the goods, is the primary EU customs valuation method. The declared amount may require additions or deductions under Union Customs Code rules.

For a typical shipment from China, the customs value may include:

Goods value: The commercial invoice value, subject to customs valuation review.

Freight to the EU border: International transport costs up to the point where the goods enter the EU customs territory.

Insurance: Cargo insurance relating to transport up to the EU border.

Dutiable additions: Packing, assists, royalties or commissions may need to be added when the valuation rules require them.

Incoterms affect which costs are already included. A FOB invoice normally requires international freight and insurance to be added. A CIF invoice may already contain those amounts. A DDP price should be separated into goods, freight, taxes and post-import delivery costs before the customs value is reviewed.

Customs Duty and Import VAT Formulas

The calculation sequence is:

Customs Duty = Customs Value x TARIC Duty Rate

Import VAT = VAT Taxable Amount x Applicable VAT Rate

The VAT taxable amount generally includes the customs value, customs duty, other import taxes and eligible incidental expenses. Depending on the circumstances, transport and insurance to the first destination in the importing member state may also be included.

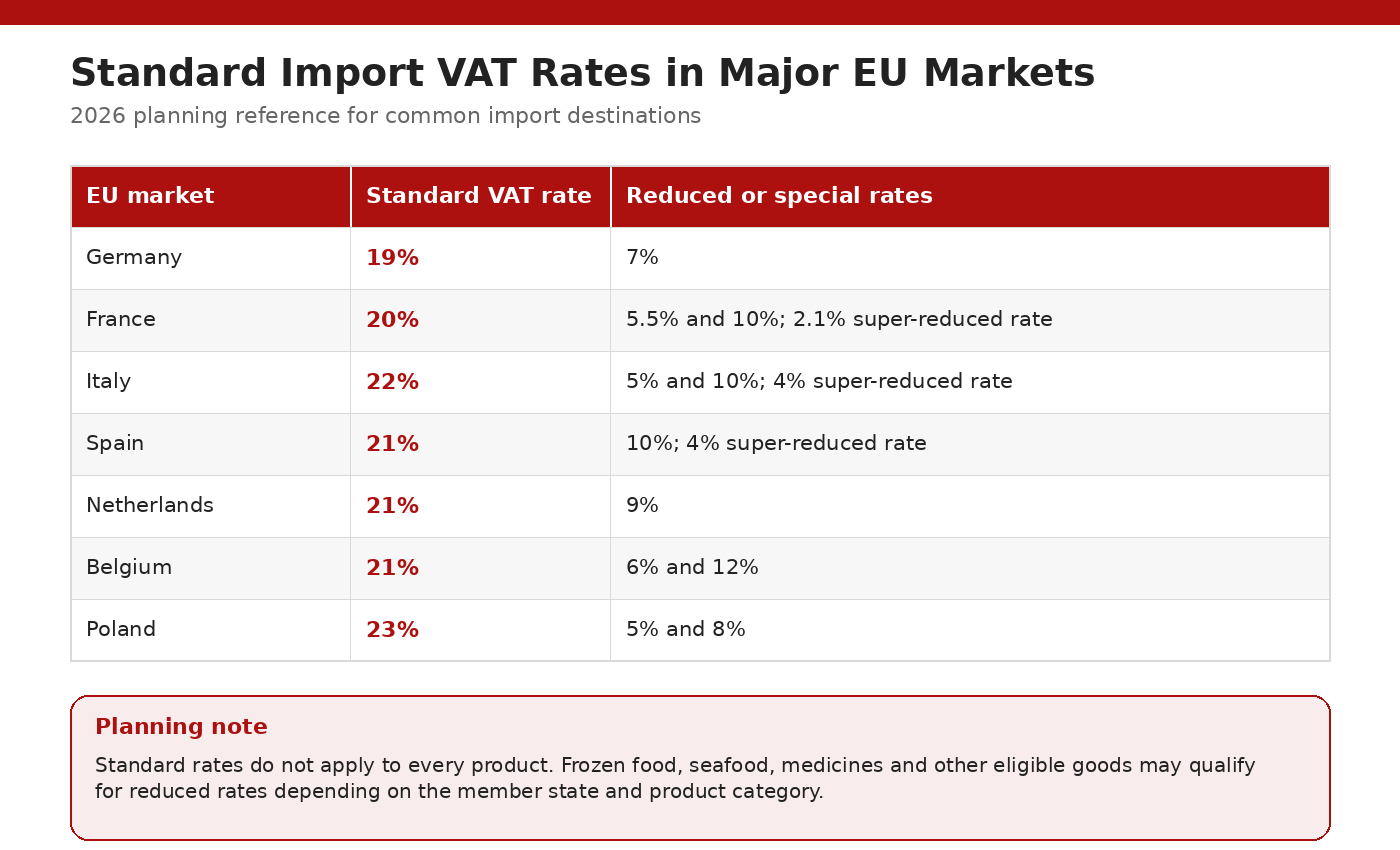

Standard Import VAT Rates in Major EU Markets

Import VAT is charged at the rate applicable in the member state where the goods are released for free circulation. The standard rate applies to most products, while food, medicines and other eligible categories may qualify for reduced or special rates.

How HS, CN and TARIC Codes Determine the Duty Rate

A supplier's six-digit HS code is only the starting point for an EU import declaration. The classification should be confirmed at Combined Nomenclature and TARIC level before the rate is used in a landed-cost estimate.

Difference Between HS, CN and TARIC Codes

HS code: The Harmonized System provides the international six-digit classification foundation.

CN code: The Combined Nomenclature expands the classification to eight digits for EU customs declarations and trade statistics.

TARIC code: The Integrated Tariff of the European Union adds further detail and links the goods to current tariff and non-tariff measures.

Small product differences can lead to different classifications.

A chemical may be classified according to composition, purity, concentration and use.

Frozen food can be separated by species, ingredients and preparation.

Machinery may be classified according to function, engine type or whether the shipment contains a complete unit or parts.

Where classification uncertainty has a material financial impact, an importer can apply for Binding Tariff Information. A BTI provides a legal classification decision from an EU customs authority.

How TARIC Classification Changes Import Costs

A live TARIC review may show more than the standard customs duty:

Third-country duty: The ordinary rate applied to goods from China when no preferential rate is available.

Tariff suspension or quota: Certain inputs may receive a temporary reduction or zero rate.

Trade defence duty: Anti-dumping or countervailing duty may apply in addition to the base tariff.

TARIC additional code: Manufacturer-specific rates may require a separate company code.

Import condition: Licences, certificates, restrictions or supporting document codes may apply.

CBAM coverage: The CN code determines whether the goods fall within the current CBAM scope.

A previous declaration can provide a reference, but the current shipment still requires a live review. Product specifications, tariff codes and additional measures can change.

Typical EU Customs Treatment by Cargo Category

The figures below are planning ranges based on the 2026 Combined Nomenclature. Final treatment depends on the full CN and TARIC classification, product origin and current trade measures.

The rates are based on the 2026 Combined Nomenclature, which entered into use on 1 January 2026

Example: Frozen Shrimp Import Duty Calculator

The following example estimates the border taxes for one reefer shipment of frozen Penaeus vannamei shrimp cleared in Germany.

The calculation uses an illustrative 12% customs duty. Germany applies a reduced 7% VAT rate to most fish and crustaceans under Chapter 3, subject to specified exclusions. The actual CN code, duty rate and VAT treatment should be confirmed before shipment.

Commercial invoice value: The frozen shrimp has an invoice value of EUR 80,000.

Freight and insurance: International freight and insurance to the EU border amount to EUR 8,000.

Customs value: The customs value is EUR 88,000, calculated by adding the EUR 80,000 product value and EUR 8,000 freight and insurance.

Customs duty: Applying the illustrative 12% tariff to the EUR 88,000 customs value produces EUR 10,560 in customs duty.

Simplified VAT taxable amount: Adding the customs duty to the customs value creates a simplified VAT base of EUR 98,560.

German import VAT: Applying the 7% reduced VAT rate produces EUR 6,899.20 in import VAT.

Total duty and import VAT: The shipment generates EUR 17,459.20 in estimated border taxes, consisting of EUR 10,560 in customs duty and EUR 6,899.20 in import VAT.

This calculation excludes any additional transport that enters the VAT taxable amount, as well as customs brokerage, Border Control Post fees, inspections, sampling, port handling, reefer electricity, cold storage and inland refrigerated delivery.

A VAT-registered business may be able to deduct eligible import VAT through its VAT return. Customs duty normally remains part of the landed cost.

Anti-Dumping Duties on Chinese Goods

Anti-dumping duty can be charged in addition to the ordinary customs tariff. The measure may use a percentage of the CIF price, a fixed amount or another calculation defined in the relevant regulation.

This can materially change the cost of chemical imports. In 2026, the European Commission imposed anti-dumping duties of 29.1% to 42.3% on adipic acid from China and 105.6% to 113.7% on 1,4-butanediol from China. These rates apply to the defined products and producers covered by the measures.

Product Scope and Manufacturer Rates

Before using an anti-dumping rate, the importer should verify:

Product scope: Match the technical specification against the regulation, including any code marked with "ex".

Country of origin: The shipping country does not replace the legal origin of the goods.

Actual manufacturer: A trading company name cannot establish eligibility for a producer-specific rate.

Additional code: Declare the correct TARIC additional code where the measure requires one.

Invoice wording: Some company-specific rates require a prescribed commercial invoice declaration.

Measure status: Check whether the duty is provisional, definitive, under review or approaching expiry.

Any applicable duty should be included before the order is approved. A low supplier price can become commercially unworkable when a high residual rate applies.

CBAM Costs for Imports from China in 2026

The Carbon Border Adjustment Mechanism entered its definitive phase on 1 January 2026. It currently covers selected CN codes in the cement, iron and steel, aluminium, fertiliser, hydrogen and electricity sectors.

Products Covered by CBAM

CBAM coverage follows the CN codes listed in the legislation. A finished product containing steel or aluminium is covered only when its own classification falls within the mechanism.

This distinction matters for chemicals and machinery. Certain fertilisers are covered, while many solvents, paints, adhesives and finished machines remain outside the current list.

The Annual 50-Tonne Threshold

Importers bringing in covered goods other than hydrogen and electricity below the annual 50-tonne single mass threshold are exempt from the principal CBAM obligations. Importers of hydrogen and electricity follow separate threshold treatment.

The threshold is assessed across the calendar year. Importers should monitor cumulative volume across shipments and customs representatives.

2026 Reporting and Certificate Obligations

For 2026 imports above the applicable threshold, the importer needs to prepare for:

Authorised status: The importer or qualifying indirect customs representative must hold authorised CBAM declarant status.

Embedded emissions data: The file must contain emissions information for the installation producing the covered goods.

Annual declaration: The first annual declaration for 2026 imports is due by 30 September 2027.

Certificate purchase: Certificates for covered 2026 imports are purchased during 2027.

Certificate surrender: The certificates for the 2026 declaration must be surrendered by 30 September 2027.

CBAM exposure should be shown separately from customs duty and import VAT. The amount depends on embedded emissions, certificate prices and eligible carbon prices paid in the country of production.

Small Parcel Import Duties in 2026

From 1 July 2026, qualifying distance sales of imported goods with an intrinsic value of no more than EUR 150 are subject to a temporary EUR 3 customs duty per item. VAT remains payable, and the EUR 3 duty applies whether VAT is collected through the Import One-Stop Shop, Special Arrangements or the standard VAT process.

The charge is based on tariff classification rather than the physical quantity of identical products. Under the EU example, five T-shirts under the same classification create one EUR 3 charge, while one T-shirt and one watch create two charges totalling EUR 6. Small parcels outside the low-value distance-sale arrangement follow the normal TARIC duty and import VAT rules.

For a detailed explanation of parcel declarations, IOSS and the 2026 cost changes, see our guide to the 2026 EU customs rules for small parcels from China.

Does the EU Country of Entry Change the Taxes Payable?

The EU applies a common customs tariff, although the customs procedure determines where the goods are released and where the taxes are accounted for.

Release at the First EU Entry Point

When goods are released for free circulation at the first EU port or airport, customs duty is handled through that import declaration. The goods can then move within the EU customs territory without another import duty at each internal border.

Import VAT treatment still depends on the importing member state, the importer's VAT position and the procedure used. National postponed-accounting or deferment arrangements can change the cash-flow timing.

Customs Transit to the Destination Country

A transit procedure allows duties, taxes and commercial policy measures to remain suspended while the goods move from the EU entry point to the destination customs office.

This can allow clearance near the final warehouse or in the member state where the importer is established. The transit declaration, guarantee and discharge must be completed correctly.

Documents Needed to Calculate EU Import Taxes

Commercial invoice: Show the buyer, seller, currency, Incoterm, product description, quantity and transaction value.

Packing list: Keep quantities, packaging, gross weight and net weight consistent with the invoice and transport documents.

Freight and insurance breakdown: Separate costs to the EU border from post-entry transport and destination charges.

Technical specification: Provide material, composition, function, model and processing state.

Chemical identification: Include the chemical name, CAS number, concentration, formulation and intended use.

Food product file: Include species, ingredients, processing state and product form.

Machinery specification: Include equipment function, engine power, model, attachments and whether the shipment contains a complete machine or parts.

Manufacturer details: Identify the actual factory where a trade defence measure may use company-specific rates.

EORI number: An Economic Operators Registration and Identification number is mandatory for EU customs operations, including import and transit.

CBAM data: Provide installation and embedded emissions information for covered goods.

Origin evidence: Support the declared origin where tariff treatment or trade defence measures depend on it.

A Safety Data Sheet can support chemical and dangerous goods identification, but it does not replace a customs classification file. Transport documentation is covered separately in our guide to documentation for dangerous goods shipping.

How Gerudo Logistics Supports Your Cargo to Europe

Gerudo Logistics is specilaizes in dangerous goods, chemical and temperature-controlled shipments from China to global markets. We review available product data, transport classification, freight costs and document consistency before booking, helping importers prepare a cleaner shipment file for their EU customs representative.

Our operations cover major logistics hubs including Guangzhou, Shenzhen, Shanghai, Ningbo, Qingdao and Dalian. We coordinate sea freight, air freight, rail and door-to-door delivery for specialist cargo, including carrier acceptance, dangerous goods documentation, reefer planning and destination handover. Contact us before the freight and import cost structure is finalised.

Frequently Asked Questions About EU Import Duties

How much import duty do I pay when importing from China to the EU?

There is no single China-to-EU duty rate. The amount depends on the TARIC classification, customs value, origin and any additional tariff or trade defence measure.

Are small parcels below EUR 150 still duty-free in 2026?

No. From 1 July 2026, qualifying low-value distance-sale consignments face a temporary EUR 3 customs duty per item, while VAT remains applicable.

Is import VAT calculated on the product value or CIF value?

Import VAT normally starts from the customs value and adds customs duty, other taxes and eligible incidental expenses. The taxable amount can therefore be higher than both the invoice value and the border CIF value.

What is the difference between an HS code and a TARIC code?

The HS code provides the international six-digit foundation. The EU extends this through the eight-digit CN code and TARIC measures used for the final import treatment.

Does dangerous goods classification increase customs duty?

Dangerous goods classification affects transport compliance, carrier acceptance and freight cost. Customs duty is determined separately through the product's TARIC classification.

Is agricultural machinery duty-free in the EU?

Many soil-preparation machines, harvesting machines and agricultural wheeled tractors carry a Free conventional duty. Other machinery and tractor classifications may carry rates of around 1.7% or 7%, so the complete specification still needs review.

Can anti-dumping duty apply in addition to normal customs duty?

Yes. A covered product may carry an anti-dumping or countervailing duty in addition to the ordinary tariff, and the rate can depend on the actual manufacturer.

Conclusion

Import duties from China to Europe cannot be calculated from a supplier's six-digit HS code or a broad product description. A reliable estimate requires the EU TARIC classification, customs value, import VAT treatment, trade defence exposure and any CBAM liability.